Top-Ups and Tax Relief

Voluntary top-ups compound at CPF's ~4% and can cut your tax bill — the optimisation play, with a lock-in. (CPF Retirement Sum Topping-Up (RSTU) scheme; Inland Revenue Authority of Singapore (IRAS) relief, 2026.)

Beyond compulsory contributions, you can top up your own or a family member's Retirement Account (or Special Account before 55) under the Retirement Sum Topping-Up scheme. Two benefits stack. First, the money compounds at the Retirement Account floor of around 4% a year — well above a bank deposit, and guaranteed. Second, cash top-ups attract income-tax relief of up to S$8,000 a year for yourself and up to a further S$8,000 for family members.

Over time, the 4% compounding gap is large. Money topped up early in your career can grow into a meaningfully larger retirement income than the same sum left in a low-interest account.

The catch is lock-in. Topped-up money is committed to retirement and cannot be withdrawn before the rules allow, and the tax relief sits within your overall personal income-tax relief cap. So top up with money you are confident you will not need sooner.

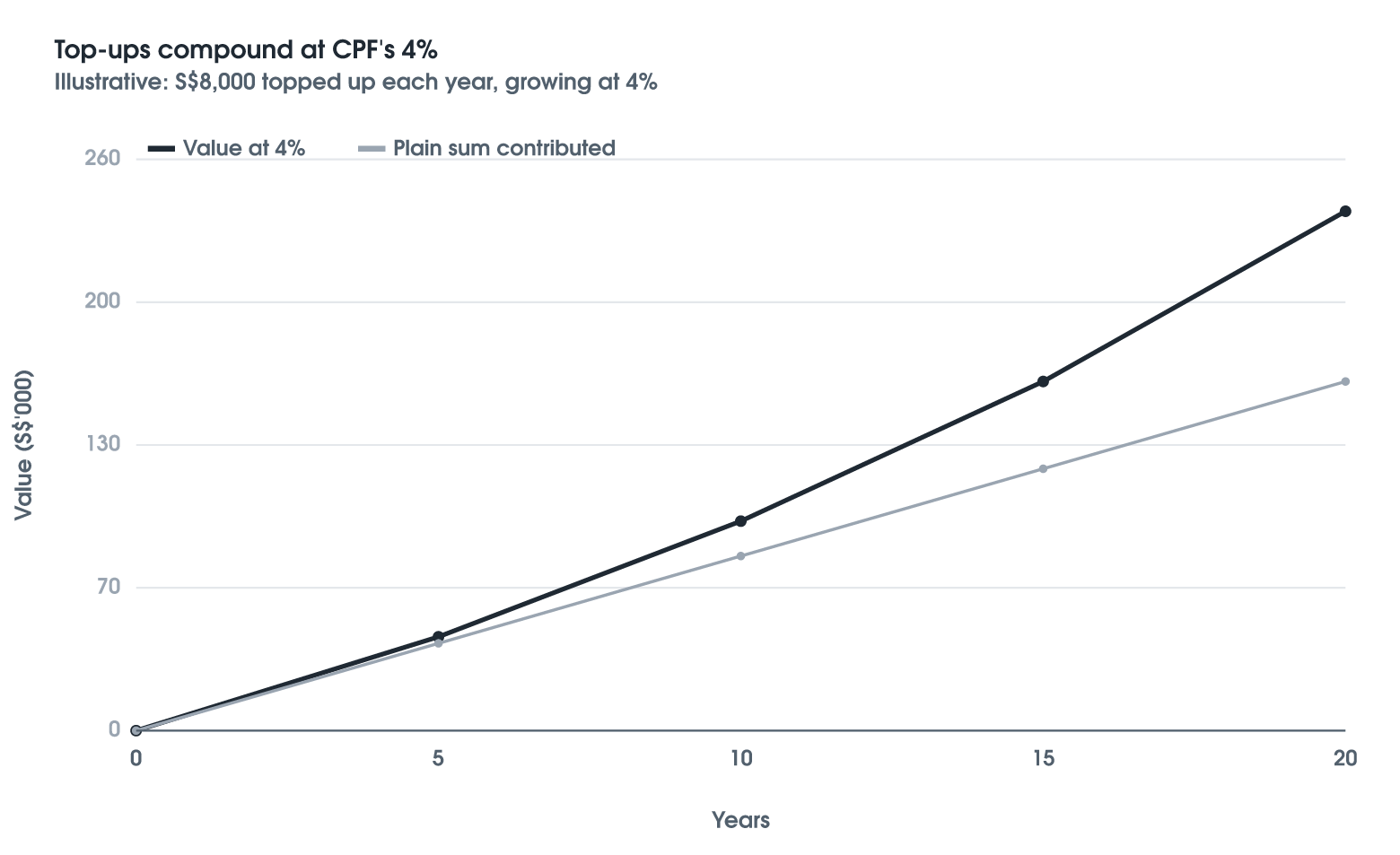

Illustrative example: the compounding gap

The chart shows an illustrative S$8,000 topped up each year, growing at 4%, against the plain sum contributed. The gap between the two lines is the quiet work of guaranteed compounding.

Relief limits and interest rates are for 2026 and sit within wider caps. Confirm current rules at cpf.gov.sg and iras.gov.sg.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.