The True Cost of Credit-Card Interest

A credit card is a brilliant way to pay and a brutal way to borrow. The trap is the gap between the two.

Used as a payment tool — spend, then clear the bill in full each month — a credit card is genuinely useful: convenient, often rewarding, and interest-free within the billing cycle. The danger begins the moment a balance is carried, because the borrowing rate is among the highest you will meet in ordinary life.

In Singapore, card interest typically runs around 26% per annum (as at June 2026; check your own card), charged on a daily basis so it compounds quickly. Worse, the "minimum payment" most cards allow is designed to keep you in debt: pay only that, and the bulk of your payment goes to interest while the balance barely moves. A few thousand dollars left to revolve can take years to clear and cost far more in interest than the original purchases.

The maths is simply unforgiving. At 26%, a debt left untouched grows by roughly a quarter every year — a pace almost no investment can match. That is why a credit-card balance is the first thing to clear, ahead of investing and ahead of most other debts: paying it off is a guaranteed, tax-free return equal to the interest you stop paying.

The rule is simple, even if the temptation is not: treat the card as cash you already have, and clear it in full, every month, without exception.

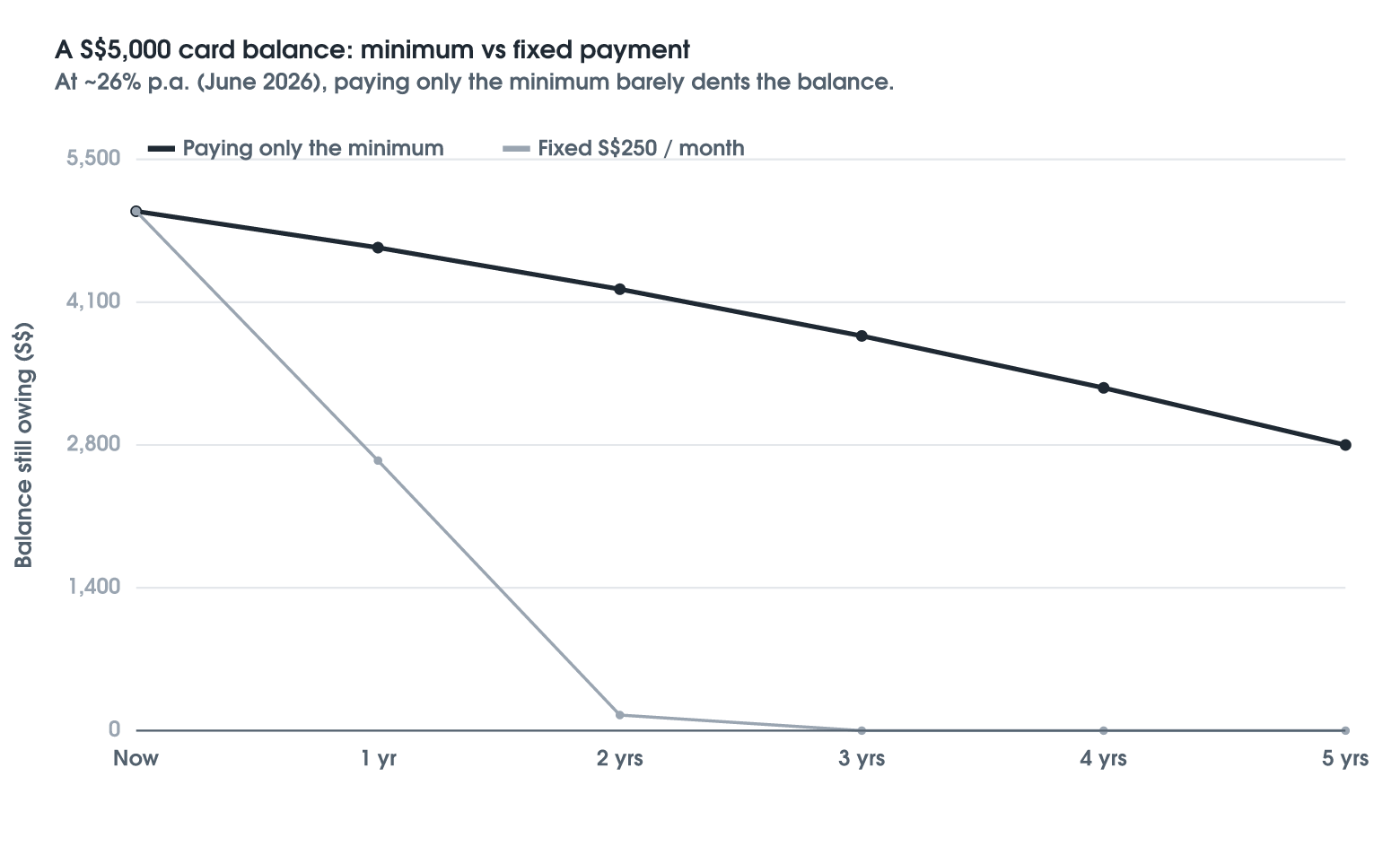

Illustrative example: paying the minimum vs paying it off

The chart tracks a credit-card balance two ways: making only the minimum payment, where the balance lingers for years, versus a fixed higher payment that clears it quickly. Same debt, same rate — the payment choice decides whether it costs you a little or a lot.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.