The 50/30/20 Rule, Explained

"Spend 50 percent on needs, 30 percent on wants, and put 20 percent toward savings." — the rule popularised by Elizabeth Warren & Amelia Warren Tyagi, All Your Worth (2005)

If you want one budget you can remember without a spreadsheet, this is it. The 50/30/20 rule splits your take-home pay — what lands in your account after tax and CPF — into three buckets: half for needs, up to 30% for wants, and at least 20% for savings and debt repayment.

Its appeal is simplicity. You do not track forty categories; you track three. Needs are the non-negotiables — housing, food, transport, insurance. Wants are everything that makes life nicer but could be paused. Savings is the slice that builds your future, and it sits at a healthy 20% by design, not as an afterthought.

The rule is a starting point, not a law, and it strains in an expensive city. For many Singapore households, especially younger ones, housing and essentials eat well past 50% of take-home pay, leaving the wants bucket squeezed. That does not break the idea — it just means your split might begin at 60/20/20, with the explicit goal of widening the savings slice as income rises.

Treat the ratios as a target to steer toward, not a rule to feel guilty about missing. The discipline that matters most is the 20% floor: protect savings first, and let needs and wants share what is left.

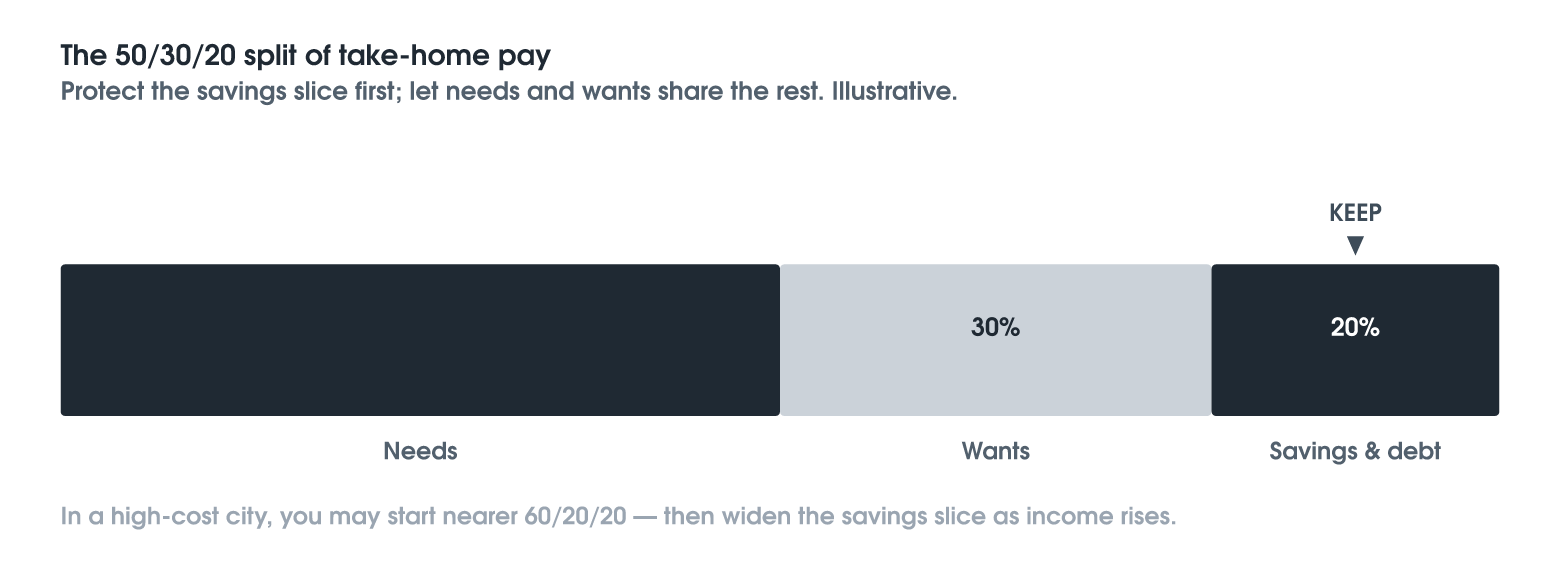

Illustrative example: the three buckets

The chart shows the canonical split of one month's take-home pay. The point is proportion, not precision — if your needs run higher today, shrink the wants bucket before you touch the savings one. Keep the savings slice sacred, and the rest of the budget can flex around it.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.