Term vs Whole Life: The Core Trade-Off

Term insures a need that ends; whole life insures one that never does. (The fork, in a sentence.)

Life insurance comes in two broad shapes, and choosing between them is the first real decision. Term insurance is pure protection: you pay a low premium for cover over a set period — say until 65 — and it pays out only if you die within that window. There is no cash value; when the term ends, so does the cover.

Whole-life insurance covers you for your entire life and builds a cash value over time, part savings and part protection. Because it must eventually pay out and holds a savings element, it costs much more per dollar of cover than term.

The trade-off is straightforward. Term gives you the most protection for the least money, which suits needs that fade — a mortgage, raising children, replacing income during working years. Whole life suits needs that never end, such as leaving a legacy or covering final expenses, and appeals to those who value lifelong certainty and a forced savings habit.

The common mistake is to buy whole life by default, paying several times more for cover you may only need for twenty years. Start from the need: temporary needs point to term; lifelong needs point to whole life.

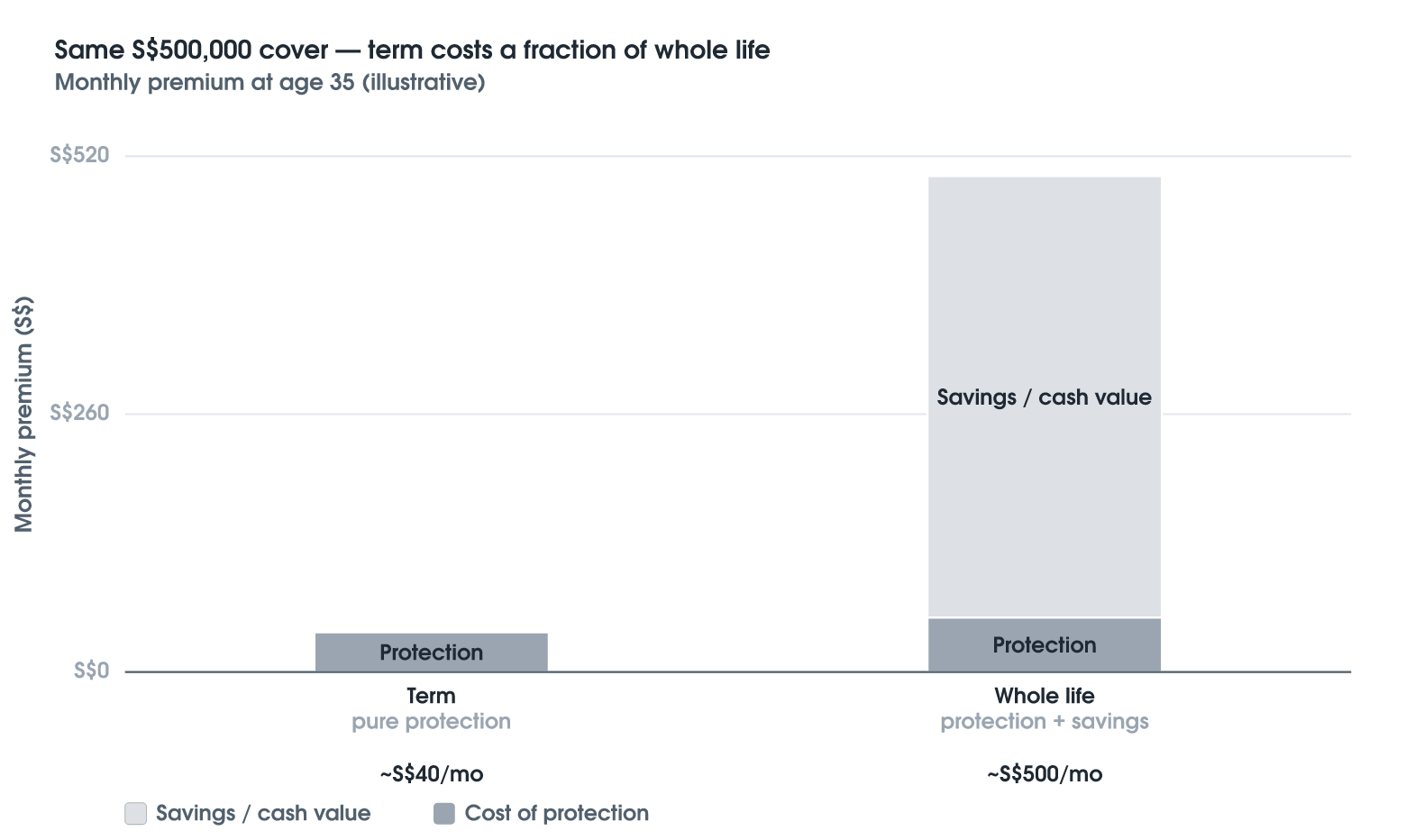

Illustrative example: two shapes of cover

The chart compares the monthly premium for the same S$500,000 of cover. Term is a fraction of the cost — pure protection. Whole life costs far more because most of the premium goes into a savings or cash-value component. That extra is the "difference" the next post suggests you could invest yourself.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.