Putting It All Together: A Retirement Framework

A good retirement plan is not a collection of tips; it is one ordered framework. (Pulling the pillar together.)

Each of the other posts in this pillar tackles one piece of the puzzle. This one connects them into a single sequence you can follow — from "still working" to "drawing an income". Five steps, each building on the last.

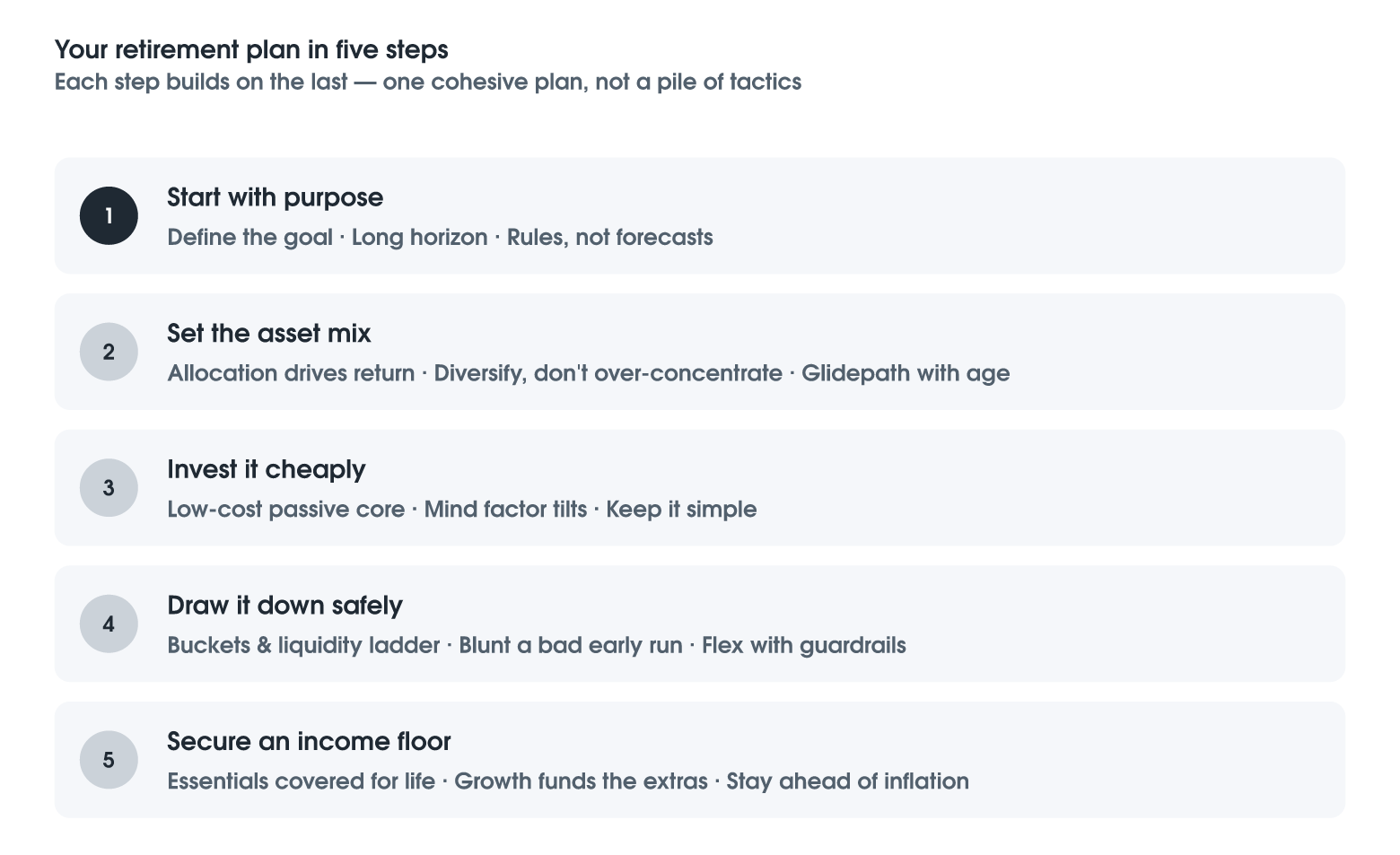

1. Start with purpose. Decide what the money is for — essentials, lifestyle, and perhaps a legacy — before choosing any investment. Then adopt a long-horizon mindset that follows written rules rather than reacting to market forecasts.

2. Set the asset mix. Your asset allocation drives most of your long-run return, so choose it deliberately. Diversify across asset classes, avoid over-concentrating in any one thing — a single property, employer, or market — and ease your equity share down gradually as you age (the glidepath).

3. Invest it cheaply. Most active funds lag their benchmark after fees, so build a low-cost, mostly passive core. Understand any factor tilts you take, and treat complicated "alternative" products with healthy scepticism.

4. Draw it down safely. Hold your near-term spending in buckets, or a liquidity ladder, so a bad run early in retirement never forces you to sell investments at the bottom — the danger known as sequence risk. Use a sensible withdrawal rate as a guide, smooth the amount you draw, and flex within guardrails when markets move.

5. Secure an income floor. Cover your essential spending with income you cannot outlive, keeping market falls away from the basics — while growth assets fund everything above the floor and help you stay ahead of inflation over time.

Illustrative example: the plan in five steps

The chart lays out the sequence and the key idea inside each step. You do not need to act on everything at once — start with purpose and the asset mix, and the rest follows. The aim is coherence: a plan whose parts pull in the same direction, decided in calm conditions and followed when conditions are not.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.