Lapsing and Surrender: The Hidden Cost of Quitting Early

The expensive mistake is not buying the wrong policy — it is buying the right-sounding one and abandoning it early. (Where the loss hides.)

When you take out a cash-value policy — whole life or investment-linked — the early premiums are weighted heavily toward charges and the cost of setting the policy up. As a result, the cash value builds slowly at first. Surrender in the first several years and you typically receive back much less than you have paid in. The policy was designed to be kept for the long term, and quitting early crystallises a loss.

This matters because lapsing is common. Circumstances change, premiums become a strain, or the policy turns out to have been oversold, and the holder gives it up — at exactly the point where surrender value is lowest. The money is not stolen; it is simply lost to early exit.

The lesson runs in two directions. Before buying, be honest about whether you can sustain the premium for the full term; a policy you cannot keep is worse than one you never bought. After buying, if you are tempted to surrender, check the numbers carefully — sometimes reducing cover or pausing premiums is far better than walking away.

It is also the strongest practical argument for not over-committing to bundled policies in the first place. Cheaper, simpler cover is easier to keep — and cover you keep is the only cover that pays.

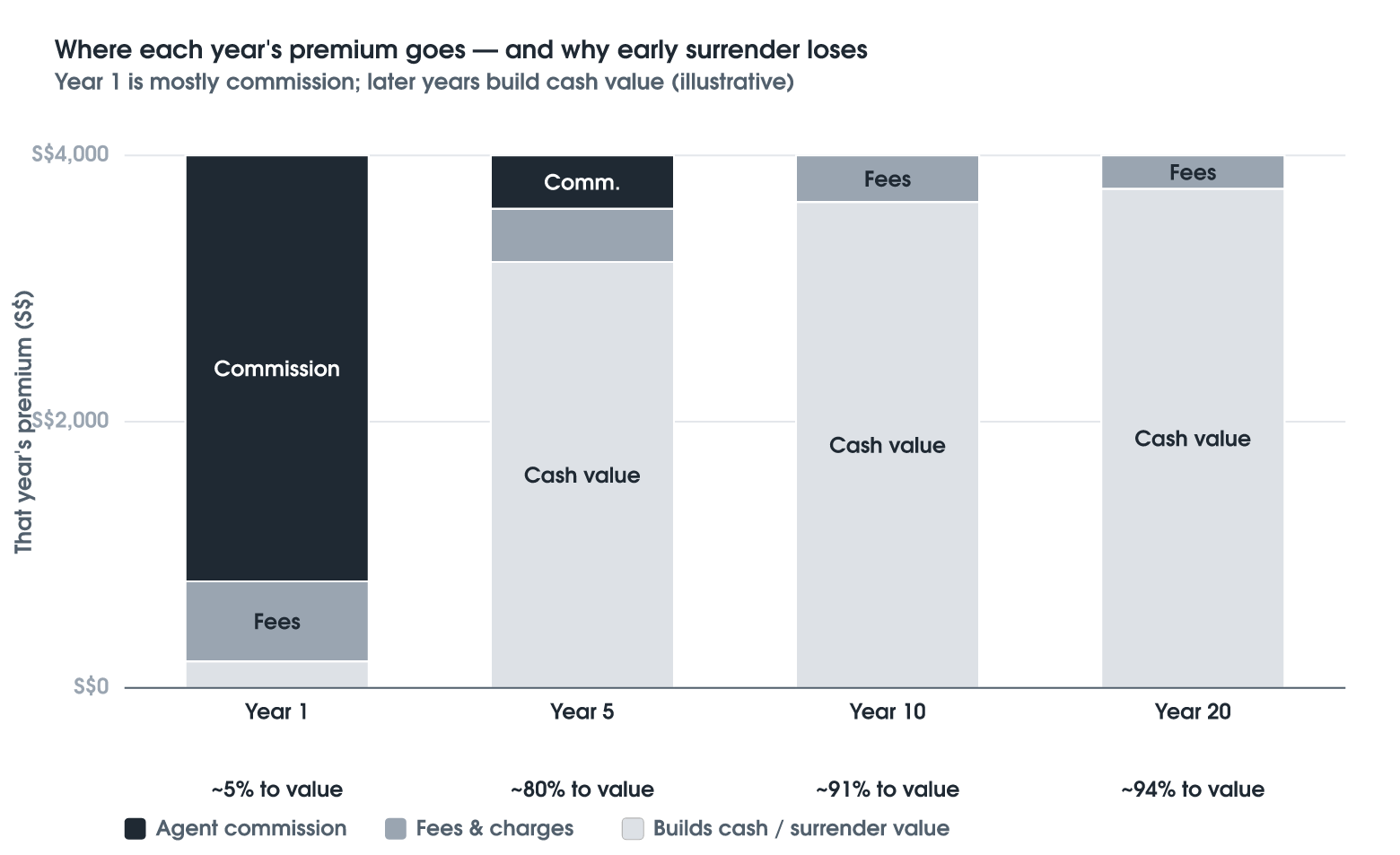

Illustrative example: surrender value versus premiums paid

The chart breaks each year's premium into where the money goes — agent commission, fees, and what is left to build cash (surrender) value. In the first year commission swallows most of the premium, so almost nothing builds value; in later years, with the commission paid off, nearly all of each premium builds cash value. That front-loading is why surrendering early returns so little — the money you paid in the early years largely never reached your cash value.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.