Integrated Shield Plans: Topping Up the Base

An Integrated Shield Plan buys you a bigger room and a wider choice — not a different illness. (What the top-up is for.)

MediShield Life covers subsidised public-ward treatment. If you want the option of a Class A ward or a private hospital, an Integrated Shield Plan tops up that base to cover the larger bills those settings produce.

An Integrated Shield Plan is really one policy with two parts: the MediShield Life layer underneath, run by the Government, and a private insurer's layer on top. You hold it with a private insurer, but the public base never goes away.

These plans come in tiers, broadly matching the ward or hospital you want access to — from higher public wards up to private hospitals. The higher the tier, the wider the choice and the higher the premium.

Premiums rise steeply with age and tier. MediSave can pay the MediShield Life portion in full, and the private portion up to set yearly limits (the Additional Withdrawal Limits), but above those caps the balance must come from cash — a cost that grows as you get older.

Choosing a tier is really choosing a standard of care you would use and can keep paying for. Buying the top tier "just in case" can mean premiums you cannot sustain into your seventies — exactly when you are most likely to need the cover.

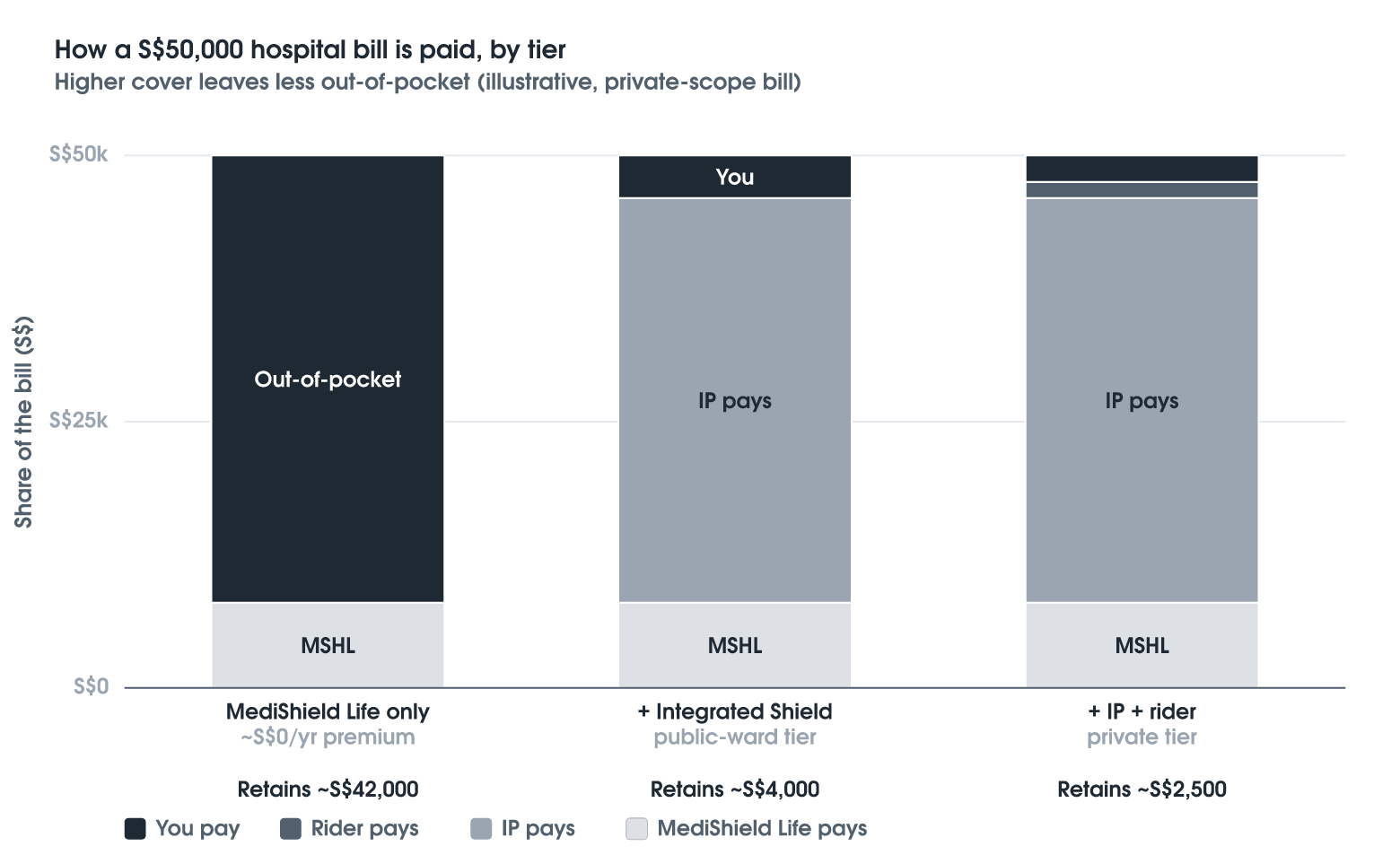

Illustrative example: base, higher public, or private

The chart takes one S$50,000 hospital bill and shows how it is paid at three levels of cover. MediShield Life sits at the base of every bar; adding an Integrated Shield Plan, then a rider, shrinks what you are left to pay — from about S$42,000 down to a few thousand. The same view sits inside the app's Integrated Shield Plan analyser, applied to your own policy.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.