Factors and the Style Box

Returns come in flavours: size, value, momentum, quality. (Building on the work of Eugene Fama and Kenneth French.)

Not all shares behave the same way. Researchers have found that certain characteristics — "factors" — have historically been linked to different long-run returns and risks. The best known are size (smaller companies), value (priced cheaply against fundamentals), momentum (recent winners), quality (steady, profitable firms) and low volatility. Fama and French formalised size and value; later work added the others.

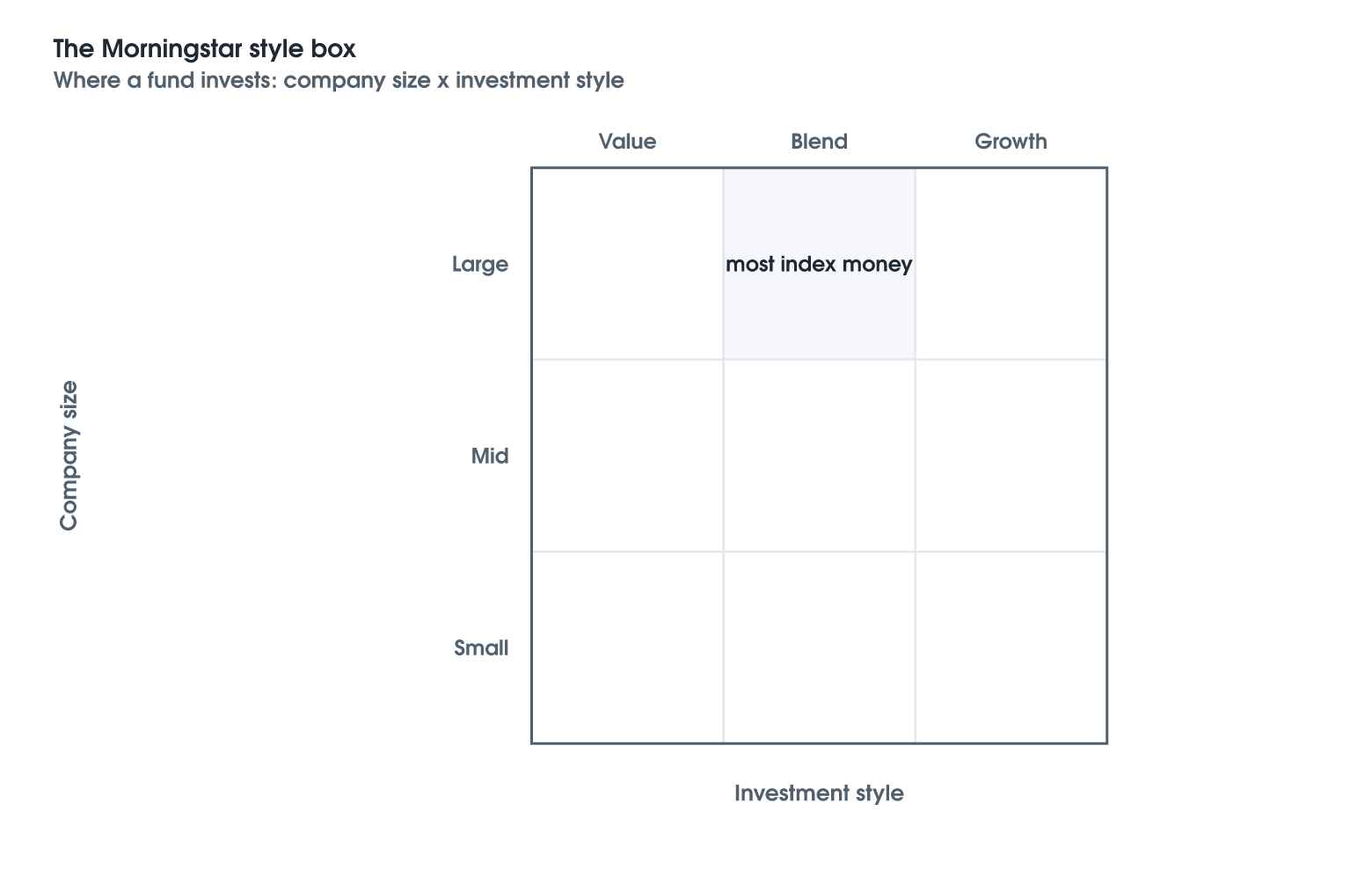

A simpler everyday map is the Morningstar style box: a three-by-three grid crossing company size (large, mid, small) with style (value, blend, growth). At a glance it shows where a fund truly invests — and whether two funds you thought were diversifying each other in fact sit in the same square.

Why it matters for a retirement pot: tilting towards a factor can change your return and risk, but factors endure long stretches of underperformance. Value lagged growth for much of the 2010s. A tilt is a deliberate, patient choice — not a free win.

Illustrative example: the style box

The chart shows the nine squares. Knowing where your funds sit helps you avoid two quiet mistakes: an accidental bet you never meant to make, and overlap that leaves you less diversified than you think. Factors are tools, not magic — understand the tilt you are taking, and hold it long enough to matter.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.