Income Protection: Insuring Your Pay Cheque

Being unable to work is often a bigger financial risk than dying — because you are still here, and still spending. (The risk people forget.)

Think of the value of everything you will earn between now and retirement. For most working adults that figure dwarfs their home and savings combined. It is their largest asset — and usually their least insured.

Income protection (also called disability income) insures that asset. If illness or injury stops you working, it pays a monthly sum to replace part of your income — commonly up to around 75% — so the household keeps running while you recover.

It fills a gap that other cover misses. Life insurance pays only on death. Hospital cover pays the medical bill. Critical-illness cover pays a one-off lump sum. None of them replaces the steady pay cheque you lose if you simply cannot work for months or years.

Two features define a policy: how much it replaces, and for how long it keeps paying — until you recover, or until a set age such as retirement. Longer payout periods and higher replacement cost more, but a policy that stops after a year may not match a long recovery.

For a single-income household especially, this is among the most important covers to hold — and among the most overlooked.

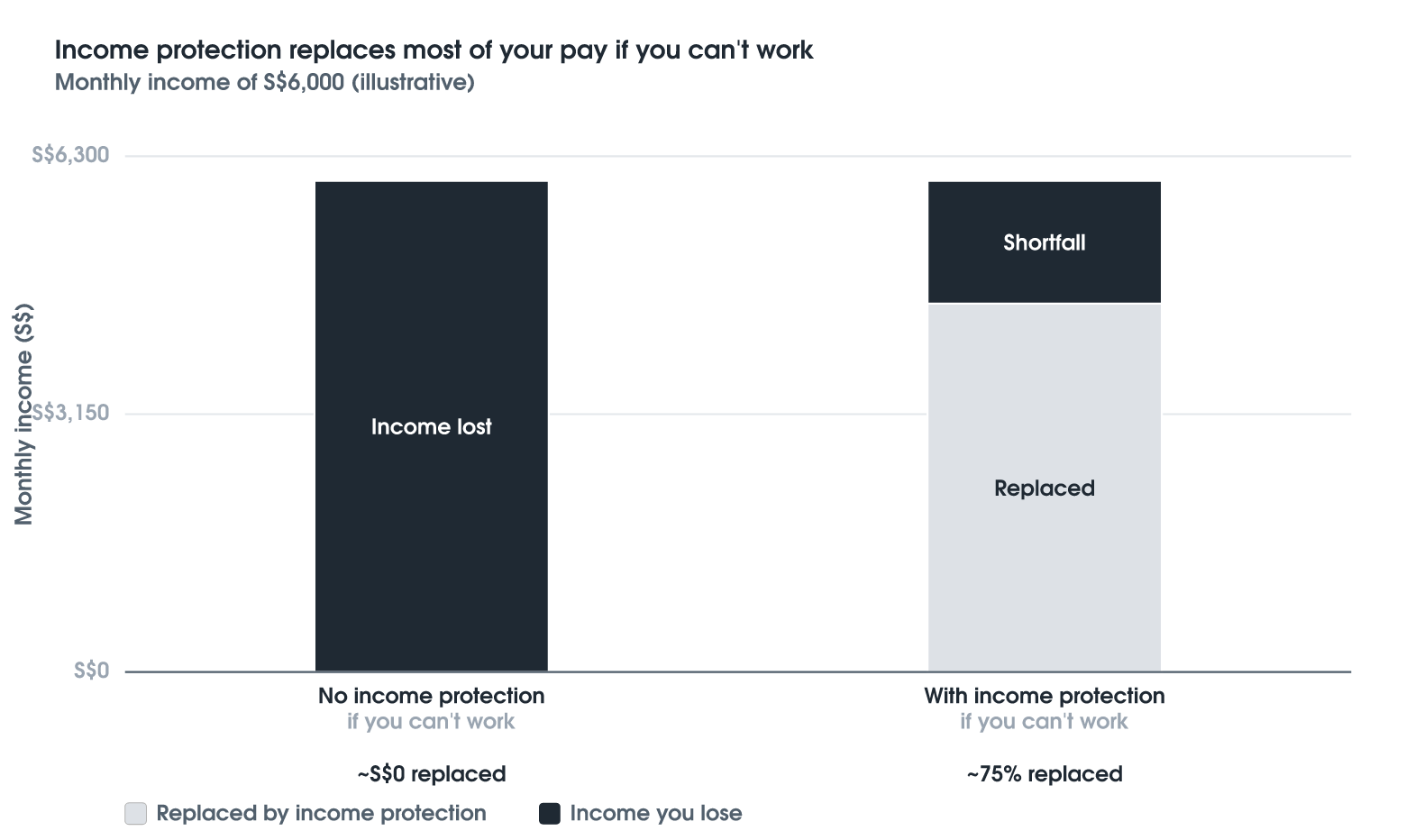

Illustrative example: what it protects

The chart compares your monthly income with and without cover. Without income protection, being unable to work removes the whole pay cheque; with it, around three-quarters is replaced, leaving a manageable shortfall rather than a cliff. It insures the asset everything else depends on — your ability to earn.

Educational only — not financial, tax, or investment advice, or a recommendation to take any particular course of action. Any names, figures, and examples illustrate a principle and are historical or simplified; past performance is not a reliable indicator of future results. Rules, tax treatment, and published figures change over time and may not reflect current policy. Wealth Diagnostics provides education and tools for financial advisers and their clients — seek licensed advice for your own circumstances before making any financial decision.